Bridging the digital divide from space

Probably one of the earliest examples of coordinated constellations of satellites is a system that we now use on an almost daily basis, every time we search for directions to our destination using applications such as Google Maps. GPS, a system that has become a standard in navigation, has its origins in a military experiment initiated by the US Department of Defence in the 1960s. At the time of the Cold War, the purpose of the GPS satellite network - the acronym stands for "global positioning system" - was to detect, locate and monitor the position of navy submarines, but later developments and extensions of the system turned it into a much more interesting product. The experiment culminated in 1993, with a constellation of 24 synchronised satellites that could position and locate objects quickly and accurately. The Russians created a very similar satellite system, known as GLONASS. A few years later, the European Space Agency (ESA) began the development of its independent - but still compatible - navigation system, known as Galileo, which offers greater accuracy and reliability thanks to its atomic clock technology and a larger number of satellites in orbit.

Megaconstellations of satellites are an evolution, a revised and improved version of these connected systems. Unlike traditional systems, which consist of at most a few dozen large and expensive satellites, megaconstellations are composed of hundreds, even thousands of smaller and cheaper satellites. In addition, these satellites are often designed to operate in lower earth orbits, which allows them to offer lower latency and higher data rates compared to traditional satellites. One of the best-known examples of mega satellite constellations is Starlink, a project developed by SpaceX, the aerospace company owned by controversial billionaire tycoon Elon Musk. Starlink aims to deploy a global network of some 42,000 satellites to provide high-speed internet access around the world. Although only some 5,800 satellites have been launched so far, if Starlink achieves its goals it could become one of the largest mega-constellations ever created. Another prominent example is OneWeb, a British company that is also building a megaconstellation of satellites to provide internet access across the globe. However, OneWeb is planning a more modest network, with just 648 satellites in low orbits. All these artificial satellites work together to form a network, a kind of giant mesh that covers the planet. In this way, when a user needs to connect to the internet, their device simply connects to the nearest satellite, sending and receiving data via radio signals that travel by bouncing around the network, between various satellites, until they reach their final destination.

These mega-constellations have numerous benefits, notably through the possibility of providing connectivity to the most remote areas of the planet. It is expected that universal access to the internet could reduce the digital divide, while at the same time reducing inequalities and improving opportunities in less developed areas through fairer access to educational and health-related resources. Indirectly, such improvements in connectivity could boost economic development in disadvantaged regions. Other multinational companies, such as Amazon, are also working on the development of their own mega-constellations - in 2023 they launched the so-called "Project Kuiper", which in addition to having satellites in orbit connects a network of antennas and fibre optics on the ground, to improve the global operation of the network - as well as other interesting projects of emerging companies such as Telesat and LeoSat. In the wake of all these developments promoted by private companies, many public institutions have considered the deployment of their own independent mega-constellations, to foster digital sovereignty and the development of infrastructures that can directly benefit the community. Recently, the European Commission announced a feasibility study related to this project, funded with more than seven million euros and with the collaboration of large companies, both in the telecommunications field and specialised in space engineering, including Eutelsat, Orange, Airbus and Thales, among others.

The main application of mega satellite constellations is, as we have seen, the development and democratisation of telecommunications, since they facilitate access to the internet and other technologies in remote areas. But they could also find very interesting applications in other areas, such as Earth observation - and therefore scientific research and the study of climate change -, the improvement of international trade infrastructures and the improvement of positioning and navigation systems.

First, the benefits of providing high-speed telecommunications services globally, including telephony, text messaging, data transmission and internet access. Megaconstellations of satellites can connect areas where traditional telecommunications infrastructure is limited or in some cases non-existent, such as rural areas, remote regions, and areas suffering from natural disasters or war. This could reduce the so-called "digital divides" that cause tens of millions of people in areas such as Latin America to be without access to high-speed internet. In these cases, the development of infrastructures such as fibre optics is often complicated due to the orography and the difficulties of access to certain isolated areas. The situation is even more worrying in other areas such as Africa and South East Asia. According to the latest available data, almost half of the world's population - 461 Tbp3T - still lacks internet access and, at the moment, only 11 Tbp3T have access to satellites that allow high-speed connections. In this regard, the OneWeb project, for example, has succeeded in connecting schools in remote areas of Alaska, Nepal, Honduras, Ecuador, Rwanda and Kyrgyzstan to the network. The new satellite systems can provide reliable internet connectivity to disadvantaged communities, bridging the digital divide and promoting digital inclusion globally. In addition, connecting these remote areas is directly linked to the growth of services for entrepreneurs and businesses in remote areas, which can boost economic and social development and improve the quality of life for millions of people around the world - provided it is marketed at affordable and accessible prices.

Another important application is Earth observation, which includes - among many other things - monitoring natural phenomena, studying environmental changes caused by the climate crisis and observing human activities around the world. With a large number of connected satellites, megaconstellations can be used to collect real-time data and high-resolution images of the Earth's surface, which can be rapidly transmitted for analysis in near real-time. One such application is reminiscent of the original purpose of GPS, as megaconstellations offer a very interesting alternative for surveillance, monitoring and management of air and space traffic. They can also mimic early weather satellites, with the potential to improve and refine the ability to prevent natural disasters such as hurricanes, floods, earthquakes and volcanic eruptions through efficient data transmission. Soon, these systems could help save lives, as well as prevent and prepare the population in time to reduce the damage caused by these catastrophic events, many believe they could be an ideal solution for providing emergency communication services in crisis situations. In this sense, other environmental disasters can also be prevented through monitoring, which could detect harmful activities such as deforestation, illegal mining, unregulated fishing and environmental pollution at an early stage, helping to protect the environment and promote global sustainability.

This technology is also expected to have a major impact on other sectors. For example, in the field of precision agriculture, coordinated and interconnected satellite data can help in the control and monitoring of crops, facilitate yield prediction and improve resource management. Thanks to the high speeds offered by megaconstellations, it will also be possible to implement more efficient systems for higher density data collection, which is extremely valuable in big data and artificial intelligence, which will enable real-time decision-making for the improvement of agricultural activities. This data can include early warnings about pests and adverse weather conditions, which will allow for better management of resources - water, fertilisers, pesticides, labour - and ultimately increased productivity. Similarly, these monitoring applications can find applications in the study of weather and climate. According to institutions such as the US National Oceanic and Atmospheric Administration (NOAA), megaconstellations will make it possible to monitor the health of our planet by observing the evolution of forests, the retreat of glaciers or air and water pollution in real time. These data will also contribute to the scientific acquis and will facilitate a better understanding of climate, animal migration patterns and other global phenomena that, at present, seem too complex to understand and model with current systems. In short, mega satellite constellations have a wide range of potential applications and uses, far beyond telecommunications. These satellite systems - like 5G, the internet of things and other technologies - are changing the way we interact with technology and the network through more accessible and efficient connectivity.

Despite all these advantages, the development of networks of hundreds - even thousands - of artificial satellites poses several problems. One of the main problems is the congestion of the Earth's orbit, which can increase the risk of collisions between satellites, which in turn generate space debris and can lead to accidents as a result of debris re-entering the atmosphere. As more satellites are launched into space, the risk of collisions not only with other satellites in orbit, but also with manned spacecraft and space stations is also increasing, which is extremely dangerous for the missions but, above all, for the astronauts. In addition, the accumulation of space debris in orbit can make access to space more difficult and increase the cost of space missions - the deployment of new satellite networks could be complicated by existing networks, a catch-22. This is known as the "Kessler effect": as the density of satellites, spent rockets and other space junk increases, the probability of collisions increases steadily, because the fragments of a collision generate more debris, more junk, in a kind of chain reaction.

Another problem is the light pollution generated by these devices in space, as the satellites - mostly made of metal - reflect sunlight back to the Earth's surface, creating glints and bright lines in the night sky that can interfere with astronomical observations. This light pollution can not only make it difficult to observe low-luminosity astronomical objects, including stars, galaxies and nebulae, and affect astronomers' ability to study the universe, but it can also affect life on the planet by disrupting the natural cycles of light and dark, sleep and wakefulness, and affecting animal behaviour and human health. Light pollution has been shown to have a negative impact on our health, as it disrupts sleep patterns and causes stress and anxiety. Overall, this poses a major challenge for the creation of new legislation and regulation. Given the growing concern about the potential problems associated with mega-constellations, several public institutions such as the UN and the US Federal Communications Commission (FCC) are implementing regulations and standards to mitigate - or at least try to control - their negative effects. The UN is concerned about extreme cases, where a partial or total collapse of space infrastructures could take us back to the Middle Ages, even irreversibly. Institutions are now working to update and revise space legislation which, in addition to being almost 60 years old, only considers public institutions, such as NASA and ESA, but does not take into account private institutions and companies. Some of these guidelines have established requirements for public coordination and control of satellite launches and propose rules to reduce light pollution caused by megaconstellations.

Challenges of the new space economy

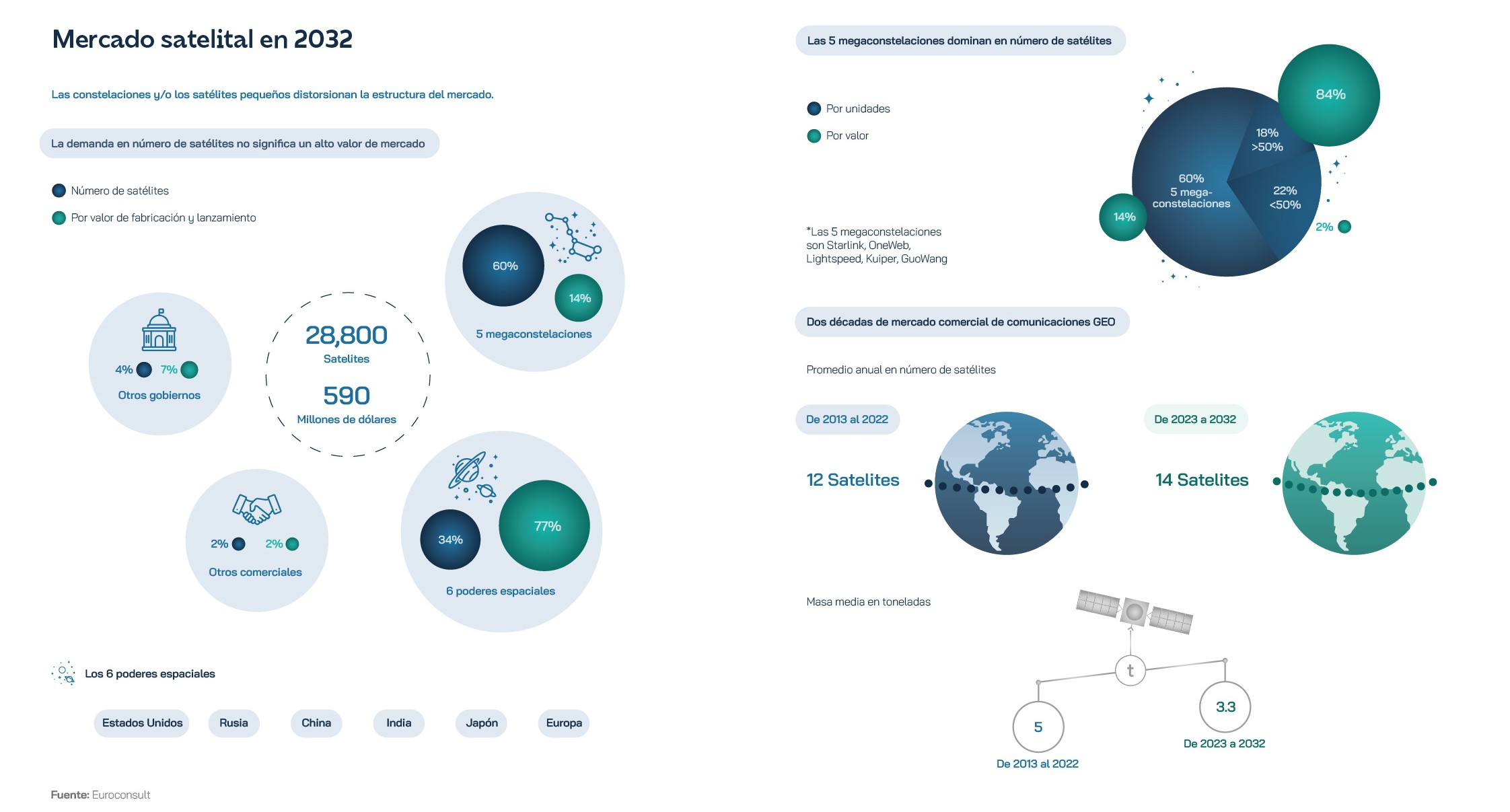

By spring 2024, Starlink had 5,399 satellites, half of all those orbiting the Earth, and although the US Federal Communications Commission had a year earlier approved the launch of 7,500, it already had another 8,086 planned and intended to apply for permits for 30,000. SpaceX carried twice as much cargo in 2023, the key metric, as the rest of the world combined last year. Its influence has begun to be felt in sectors linked to the space economy. Demand for high throughput satellite communication capacity will grow from 1.9 Tbps in 2022 to 46.1 Tbps in 2032, and the share of NGSO (Non-Geostationary Orbit) constellations will grow from 21% to 52% of that total capacity.[i]. Over the past five years, the price of global average capacity in the video and data satellite markets has fallen by approximately -16% (-3% CAGR) and -77% (-26% CAGR) respectively, and the price per Giga of data transmitted has fallen from USD 2-5 per month in 2021 to USD 0.2-1.5 in 2023. The two largest consumer broadband operators in the North American market, Hughes and Viasat, have suffered revenue declines due to new competition and the future did not look bright if they did not act. Their reaction, along with companies such as Intelsat and SES, has been to declare themselves orbit agnostic and move towards multi-orbit satellite communications offerings and strategies, and they are investing heavily in this direction.

If it continues its progress, SpaceX will achieve its goal of reaching 29,988 satellites orbiting between 340 and 614 km above the Earth by the end of the current decade. OneWeb, another of the leaders in this race, planned to launch close to 1,000 more after overcoming bankruptcy declared in 2020 thanks to the entry of Indian Bharti Enterprises and the British government into its capital. Amazon's Kuiper project planned to reach 3,236 satellites and China's Guowang mega-constellation aimed for 12,992. There is room for eccentric proposals such as that of the Rwandan Space Agency, which has presented a plan to create two constellations of almost 330,000 small satellites. Although all indications are that the Rwandan company in question, Marvel Space Communications, was planning to sell some or all of the radio spectrum rights it obtains. In total, Euroconsult estimates that more than 2,800 satellites will be launched per year between 2023 and 2032, or eight satellites per day with a total mass of four tonnes. But beyond the more or less credible announcements, and attracted by expectations of business growth, the sector is demonstrating enormous business dynamism, with eye-catching integration deals in 2023, such as the closing of the acquisition of Inmarsat by Viasat; the announcement of the merger of Echostar and DISH; and the merger of Eutelsat and OneWeb. Many satellite systems have set 2025 as the year when they will start generating revenues. Surviving to 2024, when satellite operators will end up in direct competition and downward pressure on prices will force consolidation, was seen as decisive for startups. What currently looks like a Wild West where anyone can claim their rights could have its first casualties from the end of 2024.

Despite their undoubted commercial value, the deployment of new satellite constellations will be marked by the climate of geopolitical instability. Civil and defence government operators are responsible for three quarters of the annual value of the estimated $58 billion manufacturing and launch market. The six major governments or space organisations alone (US, China, Russia, Japan, India and European governments, the EU and ESA) will account for two-thirds of total satellite manufacturing and launch demand by value. The European IRIS² system will of course include market-driven applications such as fixed and mobile broadband satellite access, satellite-enhanced networks and cloud-based services, as well as satellite links for B2B services. But it also covers a huge range of government applications for surveillance, crisis management, and connecting and protecting key infrastructure. From the point of view of frontier innovation, the EU wants to give it a leading role as a launching point for future quantum communications, through the European Quantum Communication Infrastructure (EuroQCI), included in the EU's Secure Connectivity Programme. One of its main functions will be the quantum distribution of cryptographic keys (QKD) when the technology is mature enough to be used to protect classified information.

It must ensure the viability of another key part of the European strategy, the Govsatcom programme, which focuses on communications services. At present, frequency registers are available through the International Telecommunications Union. The European Commission wants Member States to promote an open and transparent process for signing licensing agreements for the provision of government services. To do so, it is considered vital that the space assets of the Programme are launched from EU territory and that the EU owns all assets, tangible and intangible, related to the governmental infrastructure developed under the Programme, except for the EuroQC ground infrastructure. Beyond quantum technologies, IRIS² is expected to boost high-speed broadband and eliminate dead zones in communications, reinforcing the cohesion of Member States' territories. Its implementation should follow an incremental approach, starting services in 2024 and reaching full operational capacity in 2027.

Efficient public-private partnerships will be key to ensure that satellite constellations do not become a source of vulnerability for countries. In autumn 2023, SpaceX carried 13 so-called Tranche 0 reconnaissance, surveillance, intelligence and communications satellites owned by the US military's Space Development Agency (SDA). Their destination is the future Proliferate Warfare Space Architecture (PWSA) megaconstellation, the centrepiece of the CJADC2 (Joint All Dominion Command and Control) strategy. The SDA has been created to speed up space programme acquisition processes, in fact, its motto is "Semper Citius" (Always Faster). The Pentagon intends to very quickly build mega-constellations of PWSA satellite layers in low earth orbits, a new form of persistent infrared surveillance to track missiles and transmit information. The concept behind the CJADC2 initiative is to merge and share information between all branches of the military, space and the cyber network. Without a mega-constellation of satellites, this is impossible. Every two years, the SDA will acquire and launch a new tranche of satellites to cover the different layers. In September 2024, the planned Tranche 1 launches, carried on ULA (United Launch Alliance) Falcon 9 and Vuclan rockets, were to provide combat capability. Future Tranche 2 communications satellites, to be built and operated by Northrop Grumman and Lockheed Martin, will provide the transport layer.

Another example of collaboration with the business world to strengthen security has been the US Department of Defence's commissioning of Starlink to develop a military version called Starshield.[xi]capable of Earth observation, communication and customised payloads. Since these satellite constellations use laser communications, the possibility of arming them with non-kinetic space-to-Earth or space-to-space weapons to neutralise ground targets or drones cannot be ruled out, thanks to reduced atmospheric interference. The signing of the Basic Exchange and Cooperation Agreement (BECA), which gives India access to geospatial intelligence with which it can improve the accuracy of its weapons and increase its cooperation with the US, has been interpreted, in this sense, as a danger to South Asia's strategic balance. The 1967 Outer Space Treaty is limited to preventing the stationing of weapons of mass destruction in space, and there have been calls to update it to avoid militarisation, particularly of the LEO fringe.

The US government has already issued strong warnings to its partners about the risk of cyber espionage to the commercial space industry, with cases such as Russia's GPS spoofing and spoofing to hide its president's movements. Cyber-hostile operations in space are often carried out by violating the ground control system or by intercepting signals and attacking sensors, actuators or other electronic devices. In the first case, the use of cloud-based ground services, such as Amazon Web Services or Microsoft's Azure, has increased the risk of cyberattack. In the second case, remote sensors are vulnerable because the communication protocols used are based on TCP/IP models, which means that they are accessible via the internet. To reinforce security, the European Space Agency (ESA) has recently established a cyber training camp at the European Space Education and Security Centre (ESEC) in Belgium. The 6G era will bring very high-speed satellite-to-satellite links and the network will incorporate distributed decision-making, autonomous failover, resilience and scalability. Artificial intelligence will be present at all levels to make this possible.

Another key geopolitical player is China, which is building new areas for the deployment of the G60 (the name of the highway through several cities in the Yangtze River Delta region) Starlink low orbit broadband multimedia satellite network, an initiative of the Science and Technology Innovation Valley. In the first phase, 1,296 satellites were planned to be deployed, with more than 12,000 satellites to be added in the future. Tencent's G60 intelligent computing centre will support information storage and processing. It has 800,000 servers providing 10 times more computing power than the world's number one supercomputing centre. China's other big bet is the Guowang national satellite internet plan, seen as China's answer to SpaceX's Starlink. Driven by a state-owned company set up in 2021, it includes the opening of a manufacturing centre capable of producing 300 satellites per year, with cost savings estimated at around 35%, and envisages configuring a mega-constellation of 13,000 units. The development of the small satellite sector has involved the state-owned China Academy of Space Technology, the China Aerospace Science and Industry Corporation and the Academy of Innovation for Microsatellites under the Chinese Academy of Sciences, as well as companies such as GalaxySpace and HKATG of Hong Kong.

Outside the geopolitical realm, in the purely commercial realm, mega-satellite constellations are making it possible to conceive new sectors that were unimaginable just a few years ago. For example, deep space networks (DSNs) driven by countries such as the United States, Russia, China, the European Union, India and Japan will be able to transmit information more efficiently if they can use relay satellites orbiting Mars and Earth. This has given rise to a new paradigm called the interplanetary internet and is leading to a redefinition of space networks to incorporate any type of spacecraft, from satellites to space stations or hotels, that can be used as a network node. This will also include unmanned aerial vehicles (UAVs) operating within our atmosphere, particularly in areas such as the oceans, far from the coverage of ground stations. The integration of UAVs with satellites and coastal ground base stations, to provide 5G connectivity services, fits well with the expected evolution of the global maritime industry, which may grow at a compound annual rate of around 6% until 2026. Another technology strand to be developed relates to integrated satellite internet of things (IoT) systems to offer global coverage solutions, either by providing a cost-effective solution for interconnecting internet of robotic things (IoRT) sensors and actuators, or by connecting segments of terrestrial IoT networks to IoT systems via satellite broadband to enable the internet of everything everywhere (IoEE).

On a strictly technological level, this whole revolution is leading to the consolidation of a new concept called Integrated Computing and Networking for Mega LEO Satellite Constellations (ICN-LSMC), which breaks down the barriers between computing and networking and allows for a unified management of both. It is just one of the calls for attention that are being made to the need to establish mechanisms to help orchestrate this new 'floating' ecosystem. There is even talk of a "land rush" in the radio spectrum. At the centre of the focus is the lack of operational powers of the International Telecommunications Union. At present, it needs state authorities to act as intermediaries to ensure companies' compliance with the Radio Regulations, which do not provide for an adequate mechanism to limit the proliferation of satellites in space.

While the ITU is responsible for managing the use of slots in geostationary orbit, it does not play the same role in LEO. Countries must treat frequencies as limited resources to which others must have equitable access and therefore limit their own use. But companies are not part of this market balancing mechanism and do not deal directly with the ITU. They apply for and obtain licences from their national regulator, which merely submits a general description of the mega-constellation to the ITU, including the frequencies it intends to use. And notifications to the United Nations Office for Outer Space Affairs (UNOOSA) lack enforceable compliance requirements. The 2027 World Radiocommunication Conference cycle (WRC-27) could introduce a fundamental shift in governance in favour of the greater international cooperation needed to effectively manage critical space resources. But it could also reignite the argument over multilateral mandates that has exacerbated strained international relations in recent years. At the heart of the debate is whether orbital activities should be governed by one or several institutions, and the problem is that finding common ground is becoming increasingly difficult as countries' interests in space grow.

Moreover, mechanisms such as the Equivalent Power Flux Density Limits (EPFD) in Article 22 of the ITU Radio Regulations play a key role in facilitating a dynamic market environment while ensuring interference-free operation of all satellite systems. This is a controversial issue that affects how powerful signals from non-geostationary satellites must be in order not to disrupt geostationary spacecraft activity. SpaceX and Amazon argued that the EPFD rules were obsolete in the aftermath and restricted their plans to create megaconstellations, while GEO operators such as Viasat and SES warned that changing the rules would disrupt the stability of a regulatory regime that has allowed space businesses to proliferate in recent years. WRC-23 closed in December 2023 with international regulators willing to allow technical studies to change satellite transmission power limits on the condition that no regulatory action results from them until at least 2031. They will be subject to analysis at the next RCM-27.

The issue of governance becomes particularly important when addressing the question of the huge number of objects orbiting adrift and without any function. The European Space Agency's Space Debris Office estimates that there are currently some 22,000 man-made objects several tens of centimetres in size orbiting the Earth, of which only 2,300 are functioning satellites. There is an agreement called the UN Space Debris Compendium, signed mainly by European states and organisations, which sets standards for Space Debris Mitigation (SDM). But, as in other areas related to the space economy, it is limited to disseminating information on the latest debris clearance methods, and lacks the enforcement power to impose good practice. Satellite re-entries from the Starlink megaconstellation alone could deposit more aluminium into the earth's upper atmosphere than meteorites, and could become the dominant source of high-altitude alumina. The company has announced that it will actively de-orbit its satellites at the end of their five- to six-year operational life, but that is a six-month process, so approximately 10% could be out of orbit at any time. Nearly two tonnes of Starlink satellites will have to re-enter the atmosphere daily, a far cry from the 54 tonnes per day of meteorites, but the satellites are mostly aluminium, while non-man-made space bodies average 1%. To make matters worse, the first stages of the Soyuz rockets used by OneWeb are not reusable, nor are second stage re-entries controllable, and the same is true of China's Guowang Long March constellation. In terms of sustainability, the problems also carry over to Earth. LEO megaconstellations provide substantially improved broadband speeds for rural and remote communities, but generate approximately six to eight times more emissions (250 kg CO2eq/subscriber/year) than comparative terrestrial mobile broadband. In the worst case, emissions increase by 12 to 14 times (469 kg CO2eq/subscriber/year). It is not all bright stars in the sky.

Spanish networks aim for 5G and surveillance

Innovation with a Spanish stamp has been transforming the space technology sector for several decades, with a key burst during the 1980s. It is widely accepted that terrestrial networks (TN) alone will not be able to meet the requirements of the NB-IoT (narrowband internet of things) market, forcing the search for alternative formulas given the exponential expansion of IoT applications linked to the fifth generation mobile communications network. Spanish company Sateliot launched the first four 6U nanosatellites of its future low earth orbit (LEO) constellation under 5G NB-IoT NTN standards in August 2024, aboard a Falcon 9 rocket from Vandenberg Air Force Base (California, USA) as part of SpaceX's Transporter-11 mission. It aims to extend mobile telecommunications operators' coverage to any location on the planet by integrating its satellite communications stack into Leaf Space's ground segment-as-a-service (GSaaS) network. One of Sateliot's shareholders is Indra, which, together with Enaire, is also the promoter of Startical, a company designed to put into orbit a constellation of 240 small satellites with the aim of providing services that improve air traffic management and safety worldwide.

Sateliot's drive has enabled the development of associated activities in our country, such as the actual manufacture of the satellites, which has been carried out by Alén Space, a company of the GMV group. The four CubeSat 6U nanosatellites, measuring 20x10x35 cm and weighing a net 10 kilos, have emerged from its workshops, designed to have a useful life of five years and to operate in a heliosynchronous orbit (SSO) at an altitude of between 500 and 600 kilometres. A few months before the start-up of the Sateliot constellation, in October 2023, the European launcher Vega transported nine different platforms and the first trio of nanosatellites from the National Institute for Aerospace Technology (INTA) from French Guiana, which will be integrated into the future ANSER constellation, which will be dedicated to monitoring the water quality of marshes, reservoirs, lagoons and rivers on the Iberian Peninsula.

Alén Space is part of the Deimos consortium together with Satlantis and DHV Technology. It is one of the two groups of Spanish companies to which the European Space Agency has awarded the first contracts for the development of the Spanish component of the Atlantic Constellation, one of whose promoters has been the commissioner of the PERTE Aerospace, Miguel Belló. The other successful bidder is Open Cosmos Europe, comprising Telespazio, Hispasat, ARQUIMEA and Leaf Space. The contracts are in response to the agreement signed in 2023 between Spain and ESA, which initially involved Portugal and was joined shortly afterwards by the UK Space Agency, to develop a constellation of 16 Earth observation satellites, as well as Spainsat NG, two large secure communications satellites, and the Arrakihs medium-sized scientific probe. In an initial phase, the contracted companies have consolidated the mission requirements of the constellation in collaboration with the Spanish Space Agency as end-user and ESA as supervisor.

In the field of defence, Thales Alenia Space has been working on the new SpainSat NG I and II satellites at its Tres Cantos plant (Madrid), which will provide the Spanish Armed Forces with a secure and resilient communications system, ranked among the ten most modern in the world.